At a Glance

Problem: Every invoice was treated as high risk, creating manual effort, delays, and operational bottlenecks

Role: Senior UX Designer

Scope: Internal enterprise tooling, auditing workflows, risk evaluation logic

Outcome: Reduced manual review, faster funding decisions, and improved operational efficiency without increasing financial risk

Overview

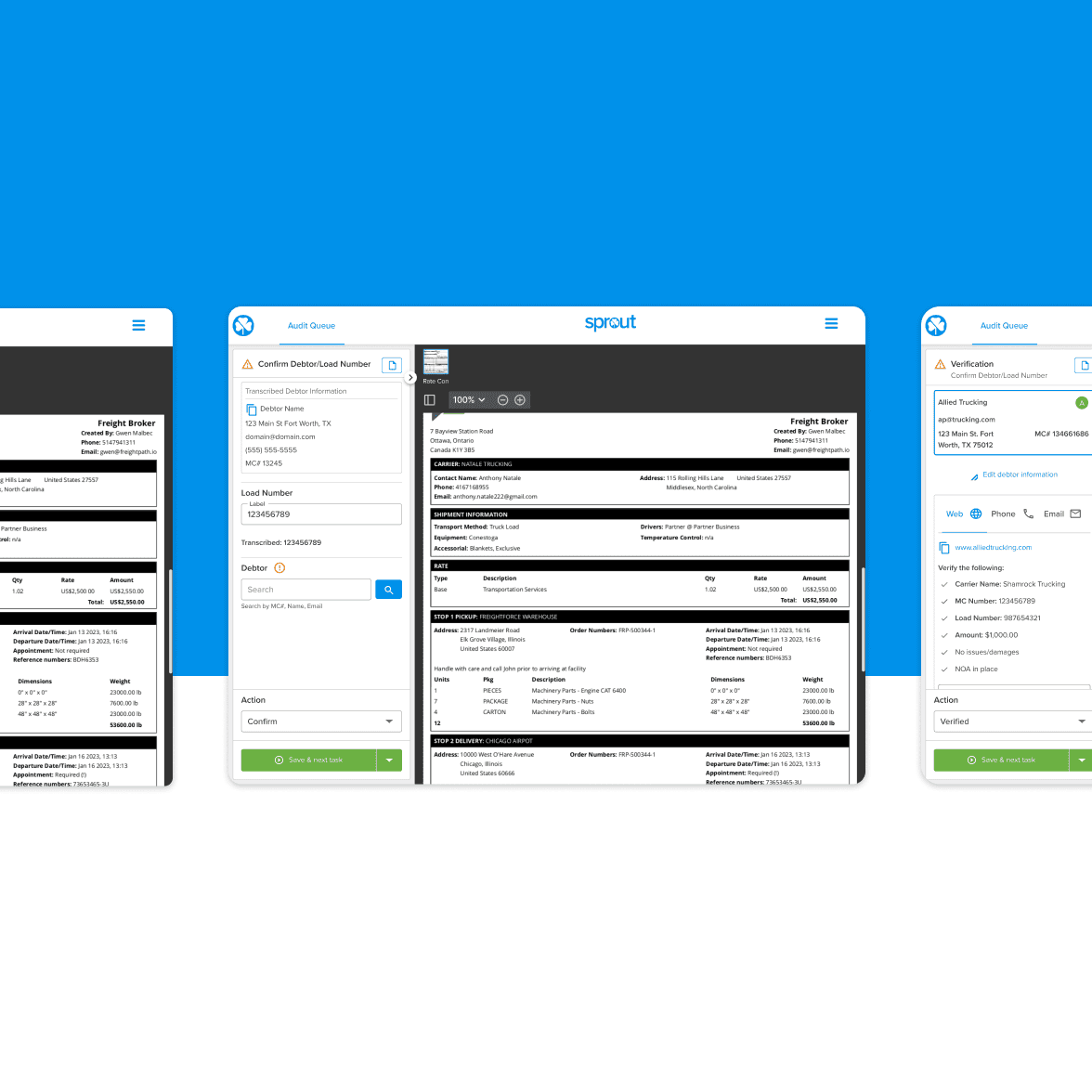

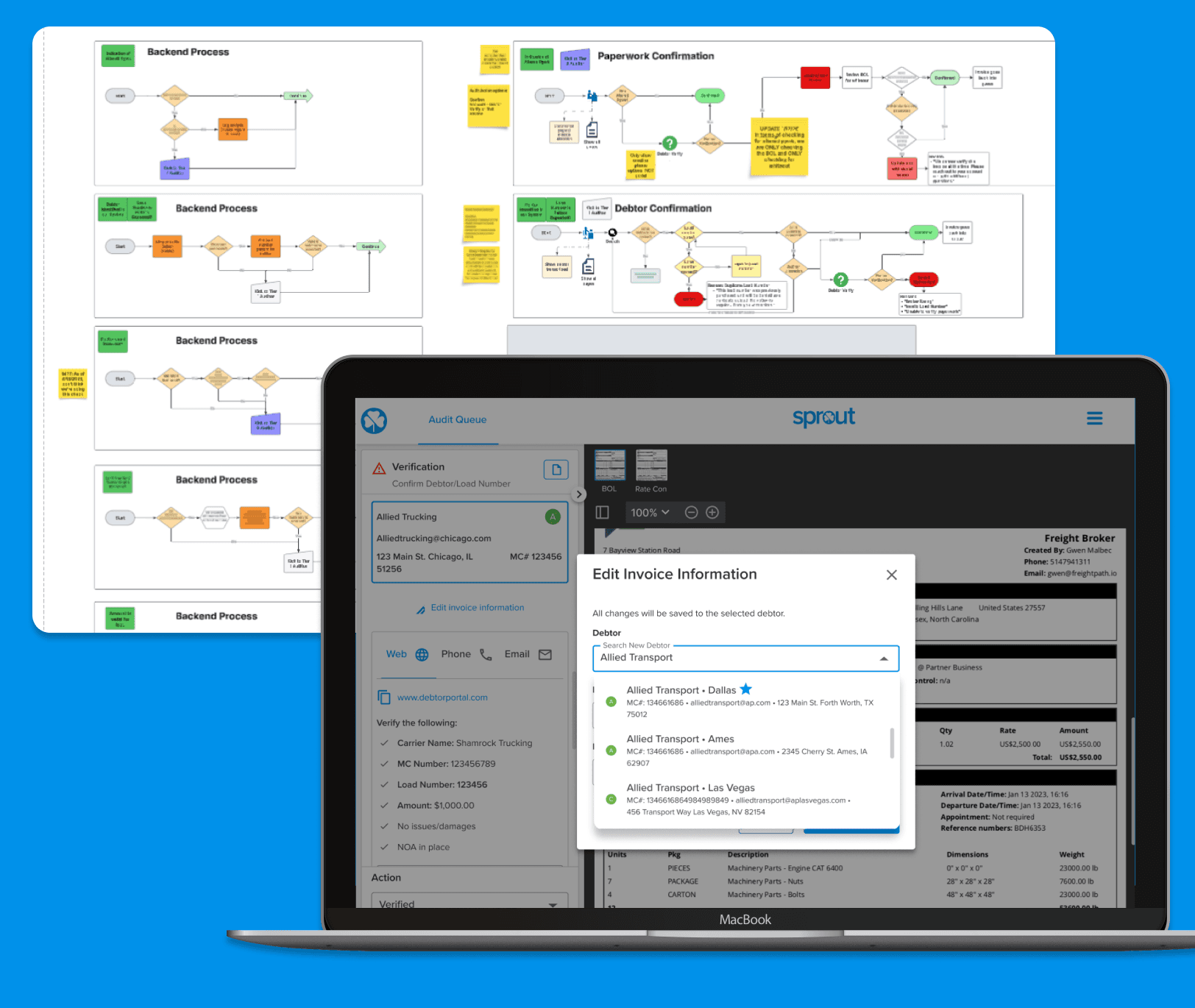

Every invoice went through the same final review before funding. That approach worked early on, but it became a bottleneck as volume increased. This project shifts that model by focusing review only where it actually adds value.

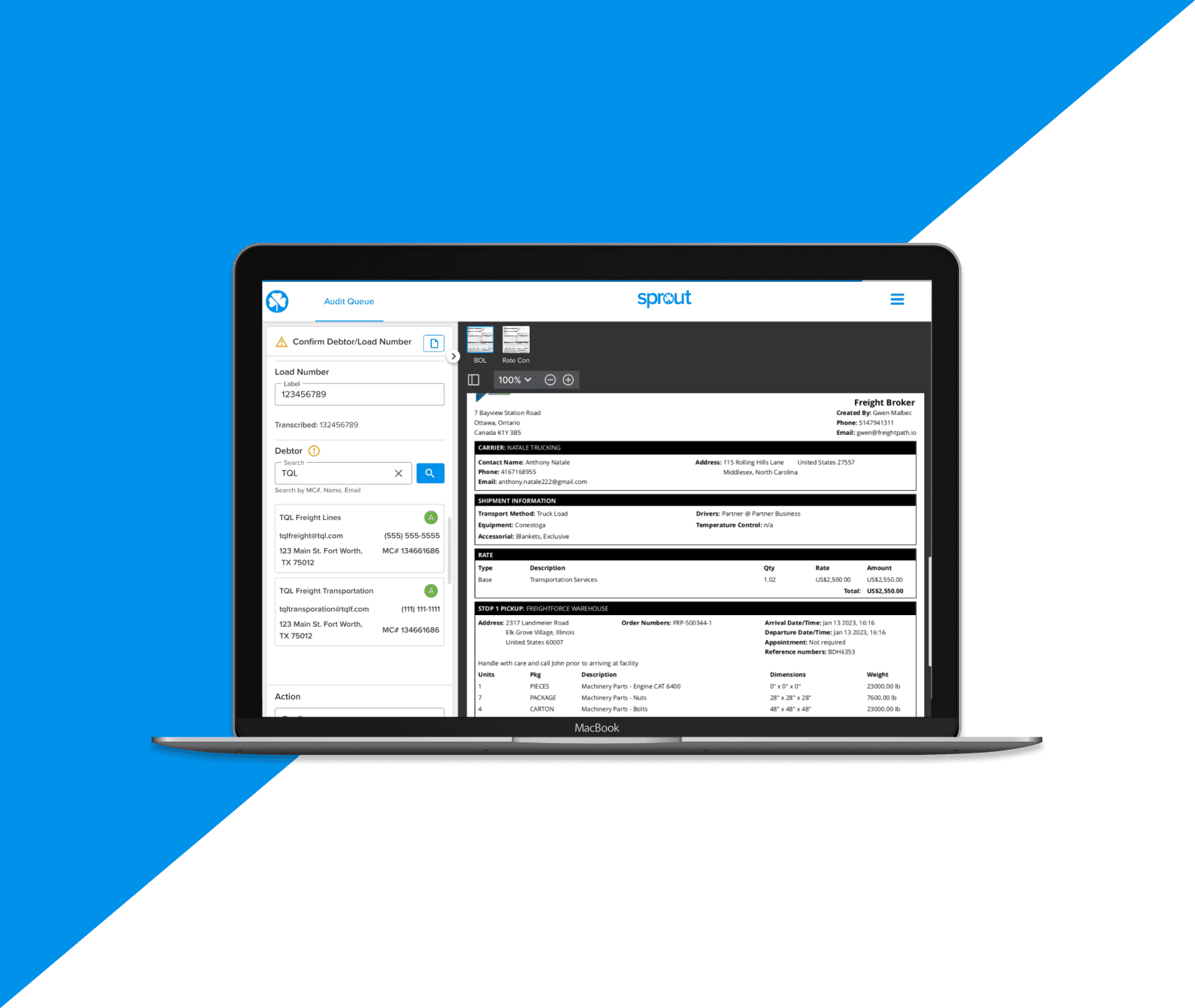

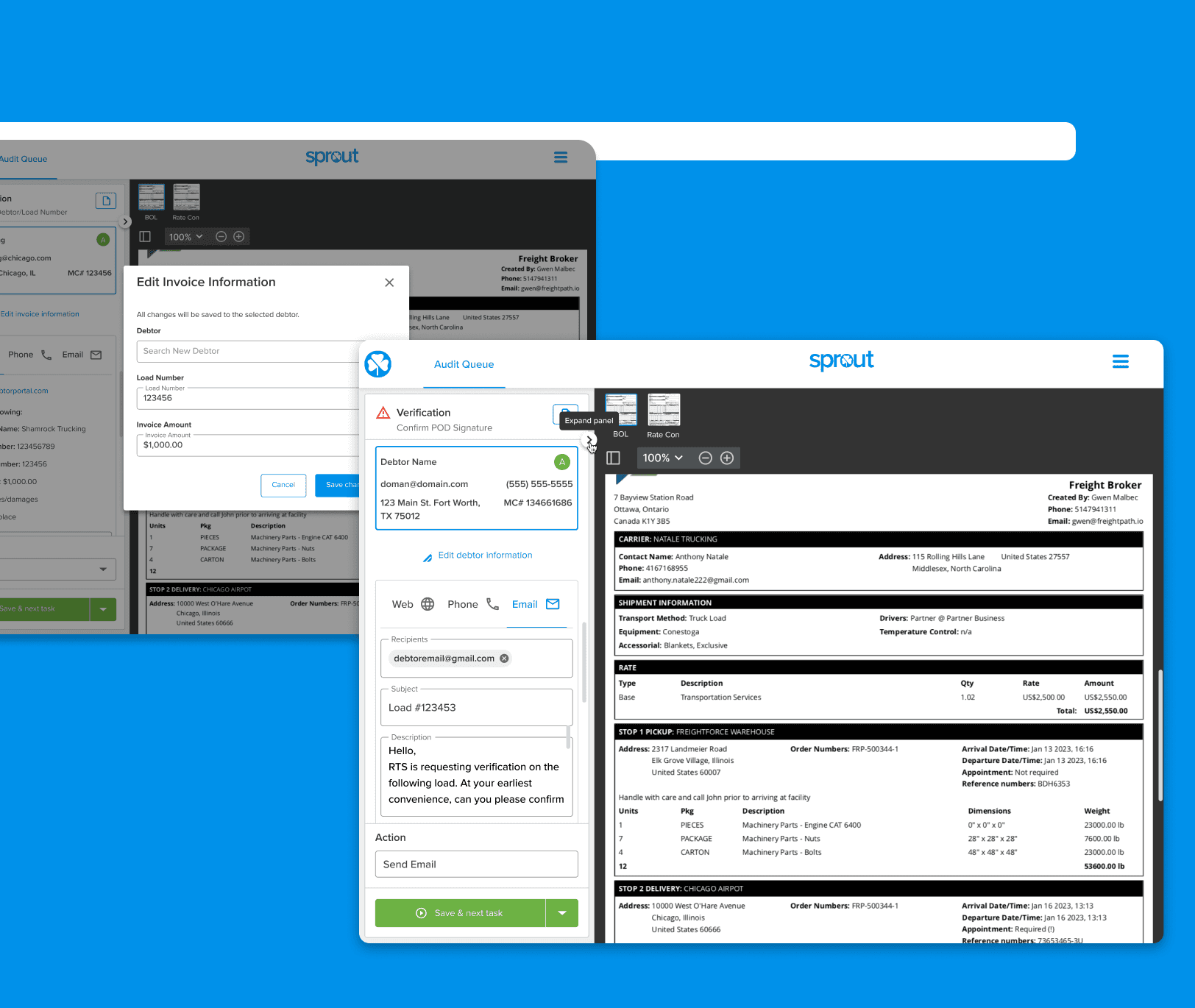

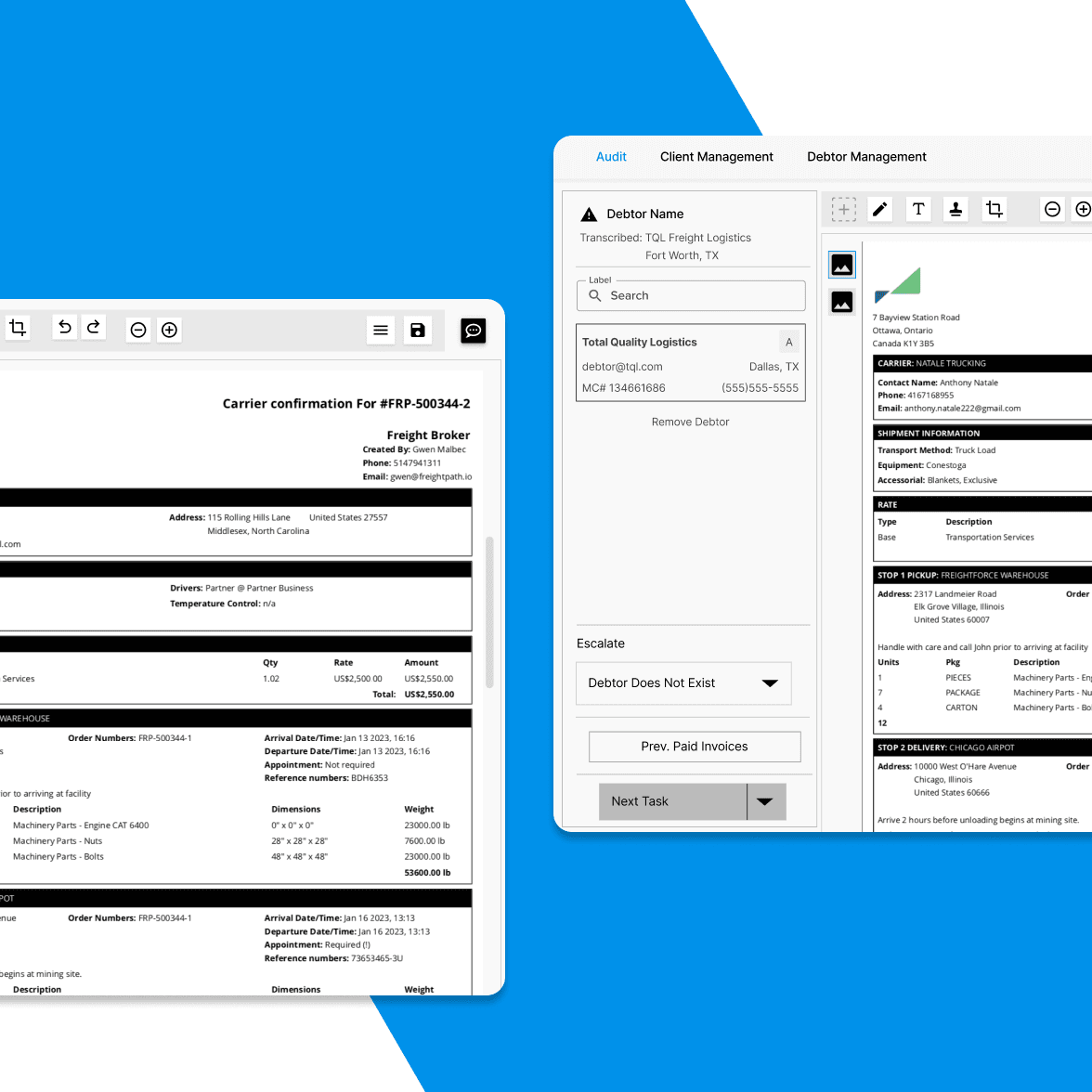

The Problem

Manual review became the default instead of the exception. Low-risk invoices were treated the same as high-risk ones, and most approvals required no action. The process stayed rigid, even though the decisions being made were not.

Defining Success

Success is less about final metrics and more about behavior. The goal is to reduce time spent on routine approvals, allow more invoices to move forward automatically, and keep decisions clear and easy to trust.

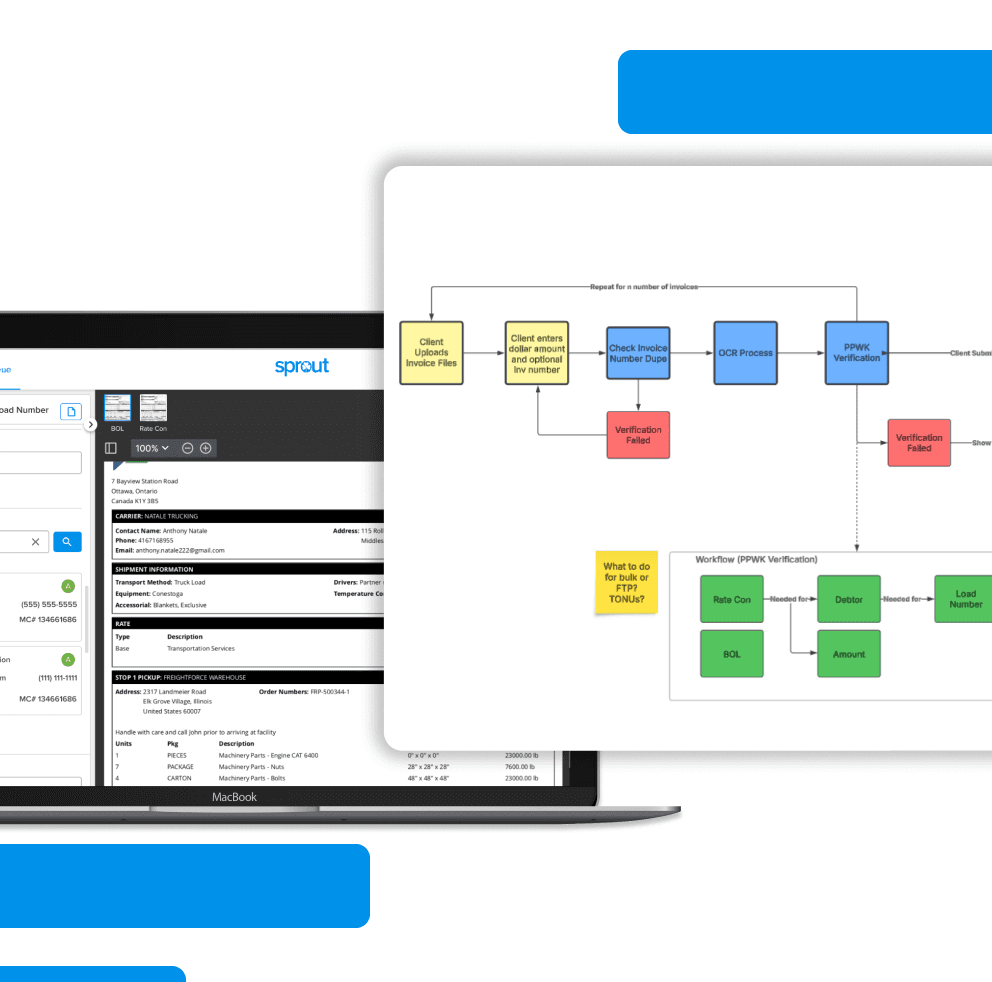

Reframing Automation Around Confidence

Rather than asking which invoices could be fully automated, we reframed the problem around risk confidence. Automation wasn’t about removing people from the process. It was about identifying when confidence was high enough to proceed without review, and when uncertainty justified human intervention.

Designing the Approach

The starting point was understanding how auditors actually assess risk in practice. Patterns showed that many reviews followed the same path and consistently ended in approval. Those patterns helped define where automation could step in without introducing new risk.

Takeaways & Next Steps

This project reinforced that automation works best when it supports judgment, not replaces it. The next step is validating impact post-launch and continuing to refine where the system steps in.

Additional Design Considerations

Designing for Edge Cases Without Slowing the Happy Path

Scaling a Shared Internal Platform